Avenue Supermart's Q4FY24 results have left brokerages impressed, painting a strong growth outlook.

Brokerages have expressed their admiration for the increase in Avenue Supermarts' store expansions, as well as the enhancement of their general merchandise and apparel offerings. JPMorgan has upgraded the stock, while Nuvama has raised its target price.

Avenue Supermarts, the company that operates the retail chain D-Mart, has reported strong earnings for the fourth quarter of FY24. The company has shown growth in profit, revenue, and profitability, which has led to a positive outlook from brokerages.

They are forecasting a promising growth trajectory for the D-Mart operator. Additionally, the management has indicated that there will be an increasing share of GM&A in its mix, which is seen as a major positive by Nuvama Institutional Equities.

JPMorgan also views this improvement positively, as they believe that the underperformance in the apparel segment is now in the past. The foreign brokerage sees a favorable risk-reward ratio for Avenue Supermarts and believes that the business is well-positioned for acceleration.

JPMorgan has increased its rating on the D-Mart operator's stock to 'overweight' and raised the price target to Rs 5,400, showing confidence in the company's future growth prospects.

Additionally, Avenue Supermarts is expected to experience positive margin effects, according to the brokerage. These effects will stem from the advantages gained through expanding their scale, focusing on premium products, improving their product mix, and maintaining a strong emphasis on cost management. Taking all of these factors into account, JPMorgan has increased its earnings per share (EPS) projections for Avenue Supermarts in the fiscal years 2025-2026 by 3-6 percent.

Store additions fuel optimism

Nuvama is optimistic about the growth of D-Mart stores, with 24 new stores added in Q4FY24, bringing the total to 365. This marks a significant increase from the slow store addition trend seen in the previous quarters of FY24. Looking ahead, Nuvama predicts the addition of 85 more stores by FY26, coupled with a rise in GM&A share, which is expected to boost the company's margins. Nuvama has adjusted the earnings multiple to 75x PE, up from the previous 70x, factoring in the strong store addition and potential for further growth in the future. The brokerage has also raised the price target for the stock by 18% to Rs 4,821, while maintaining a 'hold' rating due to the recent sharp increase in the stock price. Meanwhile, Motilal Oswal Financial Services is impressed by Avenue Supermarts' revenue/sq ft recovery and the narrowing gap between revenue/store and revenue/sq ft, indicating an improvement in the share of large-format stores.

which is a positive factor.

MOFSL mentioned that these factors, combined with the decreasing inflation and the beginning of the holiday season, could potentially boost discretionary spending and lead to an enhancement in the SSSG trend. Additionally, MOFSL reaffirmed its optimistic stance by maintaining a 'buy' rating for the stock, setting a price target of Rs 5,310.

Contrarian Call

Goldman Sachs has a different view compared to the general opinion, as they anticipate Avenue Supermarts to add stores at a rate similar to the previous fiscal year, mainly concentrating on current states. Despite this, the brokerage maintains a 'sell' recommendation for the stock, setting a bearish price target of Rs 3,900. On a positive note, they acknowledged that Q4 profit growth for Avenue Supermarts has finally caught up with revenue growth.

Healthy Q4 earnings

The corporation's combined net income surged by 22.5 percent year-on-year to Rs 563 crore in the quarter. Revenue climbed to Rs 12,726.6 crore, marking a 20 percent increase from Rs 10,594 crore in the previous year. The rise in revenue was supported by the addition of new areas and enhanced productivity.

Furthermore, an enhancement in the mix of general merchandise and apparel (GM&A) contributed to a 30 basis points increase in gross margin to 13.7 percent compared to the previous year.

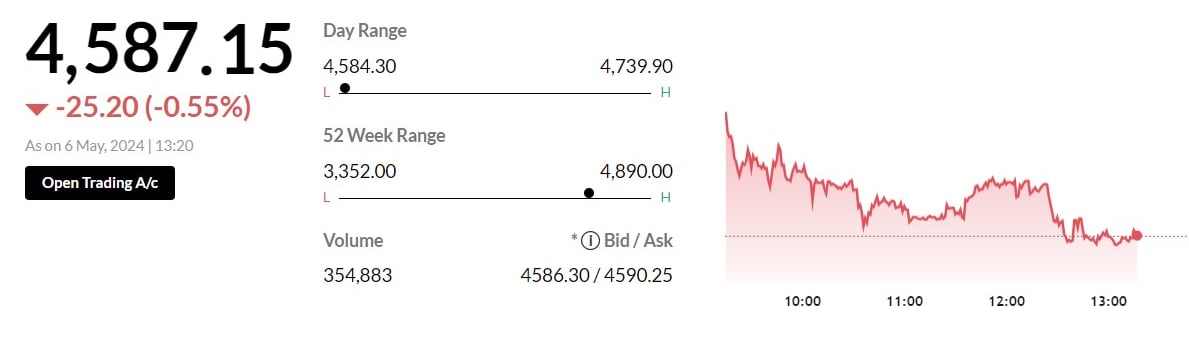

As of 09.50 am on May 6, Avenue Supermarts' shares were trading 0.6 percent higher at Rs 4,644.10 on the NSE.

Disclaimer:

The opinions and investment advice provided by investment experts on Moneycontrol.com are solely their own and do not reflect the views of the website or its management. Moneycontrol.com strongly recommends users to consult certified experts before making any investment decisions. Additionally, the company has recently experienced a significant increase in sales growth and anticipates that its profit margins have reached their lowest point.

Source: Moneycontrol.com

Connect

anzar@spaceword.in